Collateralized Loan Liquidation Risk Calculator

Collateral Loan Calculator

Calculate your liquidation risk based on collateral value and loan amount

How It Works

This calculator shows your liquidation risk based on DeFi liquidation rules.

Your current LTV ratio is calculated as (Loan Amount / Collateral Value) × 100. A ratio above the required threshold triggers liquidation.

In DeFi, liquidation fees typically range from 5-10%. This is the discount liquidators receive when they pay your debt.

For SBA loans, liquidation is handled through a slow, regulated process with multiple steps. This calculator focuses on DeFi scenarios.

Risk Analysis

Your liquidation risk based on current values

Traditional vs. DeFi Liquidation

- Slow, regulated process

- Multiple steps (appraisals, notices)

- Up to months to liquidate

- Human oversight

- Legal protections available

- Instant, automated liquidation

- Triggered by price drop

- Happens in seconds

- No human intervention

- 5-10% liquidation fee

- Portfolio-wide liquidation

- Structured waterfall distribution

- Losses absorbed by tranches

- Institutional investors only

- No direct borrower impact

When you borrow money using crypto or property as collateral, things seem simple-until you can’t pay back the loan. That’s when the liquidation process kicks in. It’s not just a bank taking your house or car. In today’s world, liquidation can happen automatically in seconds, triggered by a price drop on Ethereum, or it can take months of paperwork under federal rules. The way collateral is seized depends entirely on where the loan came from: a government-backed lender, a Wall Street fund, or a smart contract on Ethereum.

How Traditional Loans Handle Liquidation

For decades, banks and government agencies have used a slow, regulated system to recover money when borrowers default. The U.S. Small Business Administration (SBA) 7(a) loan program is one of the most tightly controlled examples. If a small business can’t repay its SBA-guaranteed loan, the lender doesn’t just seize assets overnight. They must follow a strict checklist: get an official appraisal, try to work out a repayment plan, document every communication with the borrower, and only then move to sell the collateral-whether it’s equipment, inventory, or real estate.

The SBA requires lenders to prove they did everything possible to avoid loss. If they skip a step-like failing to notify the borrower in writing or not using a certified appraiser-the SBA can refuse to pay its guarantee. That means the lender eats the loss. The National Guaranty Purchase Center in Virginia handles all these cases. Lenders report monthly using Form 1502, and when a loan is finally paid off or written off, they send an email with code "6" to update the SBA’s system. There’s no automation here. It’s all paper trails, legal notices, and waiting periods.

Florida, like other states, enforces these federal rules. Defaulting on an SBA loan doesn’t just mean losing your business assets. It can lead to personal lawsuits, credit damage that lasts years, and even disqualification from future government loans. The goal isn’t punishment-it’s recovery. Every step is designed to maximize returns while protecting both lender and borrower from unfair practices.

What Are CLOs and How Do They Liquidate?

Collateralized Loan Obligations (CLOs) are complex financial products that bundle hundreds of corporate loans into tranches sold to institutional investors. Unlike personal or small business loans, CLOs aren’t meant to be repaid by one borrower. Instead, they rely on cash flow from dozens, sometimes hundreds, of companies paying interest on their loans.

A CLO has three main phases. First, the reinvestment period-usually up to five years-where the manager buys and sells underlying loans to boost returns. Then comes the non-call period, where investors can’t force a payout. Finally, the amortization phase: cash from loan payments flows down to investors, reducing the debt over time.

Liquidation in CLOs doesn’t mean seizing a single asset. It means the entire portfolio is wound down. If a company in the pool defaults, the loss hits the lowest-rated tranche first-the equity layer. Higher tranches (senior notes) are protected. This structure, called waterfall distribution, has kept CLOs stable even during economic downturns. According to Standard & Poor’s, post-2008 CLOs (called CLO 2.0s) added extra safeguards like higher overcollateralization ratios and stricter credit criteria. These changes made them far more resilient than earlier versions.

Because CLOs are traded by pension funds, hedge funds, and insurance companies, their liquidation is handled by professional asset managers-not courts or repossession agents. When the time comes, the portfolio is sold as a whole, often to another CLO manager. The process is fast, quiet, and highly technical.

DeFi Liquidation: The Automated Version

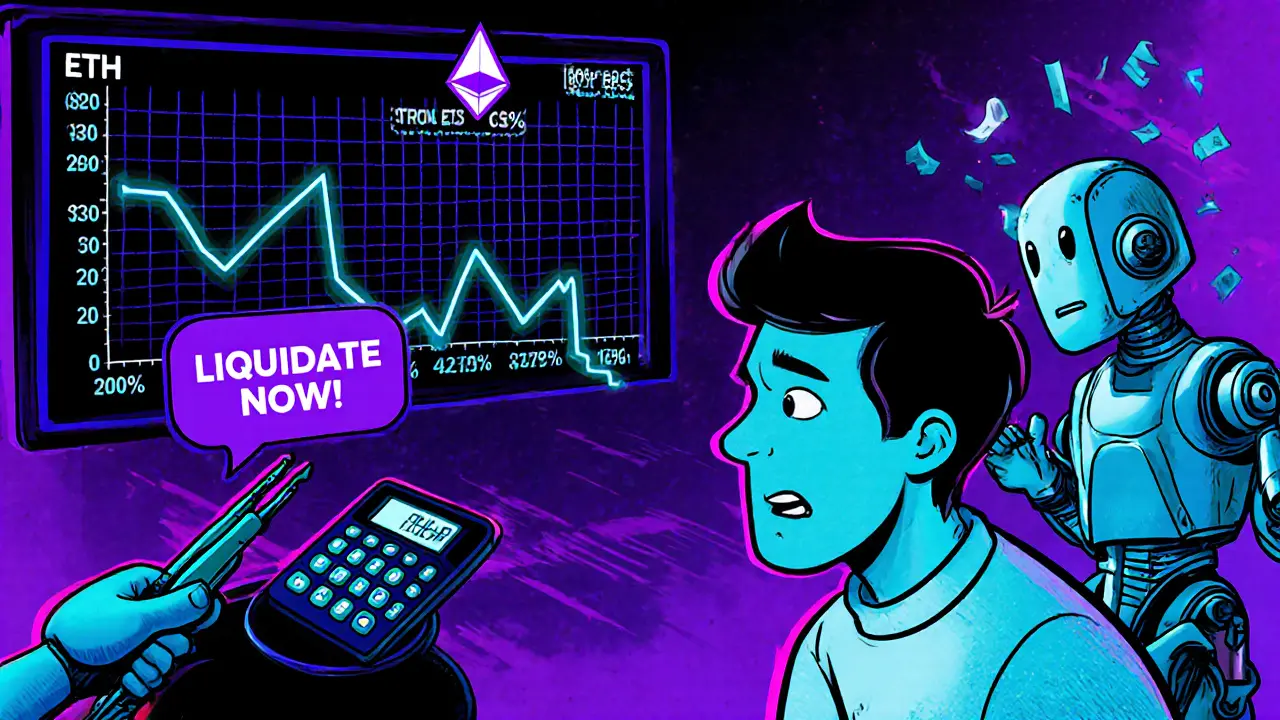

On decentralized finance platforms like Aave, MakerDAO, or Compound, liquidation is instant, public, and algorithm-driven. No human approves it. No paperwork is signed. It’s all code.

Here’s how it works: You deposit $10,000 worth of ETH as collateral and borrow $5,000 in DAI. Your loan-to-value ratio is 50%. Most protocols require you to stay above 150% collateralization. If ETH drops 40% and your collateral falls to $6,000, your ratio hits 83%-below the 110% safety threshold. At that moment, a smart contract triggers a liquidation.

A liquidator-a person or bot-steps in and pays off your debt in DAI. In return, they get your ETH at a discount, usually 5% to 10% below market price. That discount is the liquidation fee. But here’s the catch: if the fee is too high-say 30%-no one will bother liquidating. The loan stays underwater, and the protocol risks insolvency. That’s why most DeFi projects cap fees at 10%.

But even 10% isn’t always enough. In late 2023, a major DeFi protocol paused its system during a flash crash. When it resumed, hundreds of users were instantly liquidated because their accrued interest hadn’t been recalculated. The system thought they were still safe-but in reality, their debt had grown from daily yield farming fees. This wasn’t a bug. It was a design flaw: the protocol didn’t refresh debt values before checking liquidation triggers.

Today, top DeFi protocols have added grace periods after unpausing. Users get 24 to 72 hours to add more collateral or repay before liquidation runs. Some even send on-chain notifications via wallets. These fixes are slow, but they’re necessary. Automated systems can’t afford to be blind.

Why Liquidation Rules Vary So Much

The differences between SBA loans, CLOs, and DeFi aren’t accidental. They reflect the underlying trust model.

Traditional loans rely on human judgment, legal systems, and paper records. They’re slow because they’re designed to be fair. You get a chance to fix things. There are appeals, hearings, and negotiated settlements.

CLOs operate in a world of institutional investors who accept risk through structure. Losses are absorbed by layers, not individuals. Liquidation here is a financial reset-not a personal failure.

DeFi removes humans entirely. Trust is replaced by code. Speed is the priority. But that creates new risks: front-running bots, oracle manipulation, and cascading liquidations during volatility spikes. In 2022, a single ETH price drop triggered over $200 million in DeFi liquidations in under an hour. No bank could move that fast-and no bank would want to.

Each system has trade-offs. Traditional systems protect borrowers but are costly. CLOs protect investors but are opaque. DeFi protects efficiency but leaves users exposed.

What You Need to Know Before Taking a Collateralized Loan

If you’re considering a collateralized loan-whether it’s from a bank or a blockchain protocol-know this: liquidation isn’t a backup plan. It’s the default outcome if things go wrong.

- For SBA loans: Keep detailed records. Respond to every notice. Don’t assume silence means you’re safe.

- For CLOs: You won’t be directly affected unless you’re an investor. But understand that defaults in the pool can ripple through tranches.

- For DeFi: Never borrow more than 50% of your collateral’s value. Set up price alerts. Use wallets that notify you of debt changes. And never assume your collateral is safe just because the price hasn’t dropped yet-interest compounds daily.

One common mistake in DeFi? Borrowing stablecoins to buy more crypto. That’s leverage. And leverage amplifies losses. A 20% drop in ETH can wipe out 100% of your equity if you’re over-leveraged. Most beginners don’t realize that until it’s too late.

Even in traditional lending, people assume their home or car is “safe” as long as they make payments. But if your business fails, your collateral can be sold at auction for half its value. The bank doesn’t care about your emotional attachment. They care about recovering their money.

Future Trends: Where Liquidation Is Headed

The future of collateralized loans isn’t about choosing between traditional and DeFi. It’s about blending them.

Some fintech startups are building hybrid systems: using blockchain for transparency and speed, but keeping human oversight for edge cases. Imagine a loan where your crypto collateral is monitored on-chain, but a human reviewer steps in if your debt-to-collateral ratio drops below 120%. That’s the next evolution.

Regulators are also waking up. The U.S. Treasury and SEC have started asking questions about DeFi liquidation triggers. Are they fair? Are they predictable? Can users appeal? In 2025, we’re likely to see new rules requiring DeFi protocols to disclose liquidation mechanics in plain language-not just in whitepapers.

Meanwhile, CLOs are adapting to higher interest rates by shortening reinvestment periods and increasing credit quality standards. And SBA lenders are digitizing their reporting systems, moving away from paper forms to real-time API integrations.

The common thread? All systems are becoming more transparent, more responsive, and more automated. But the core truth remains: collateral isn’t just security. It’s your safety net. And if you don’t understand how it works when it snaps, you’ll be the one falling.

What triggers a liquidation in a DeFi loan?

A liquidation is triggered automatically when your collateral value drops below the protocol’s required ratio-usually 110% to 150%. For example, if you borrowed $5,000 using $10,000 worth of ETH as collateral, your ratio is 200%. If ETH crashes and your collateral falls to $5,500, your ratio hits 110%. At that point, the smart contract allows anyone to pay off your debt and claim your collateral at a discount.

Can you stop a liquidation once it starts?

In traditional loans, yes-up until the asset is sold. You can negotiate a repayment plan or refinance. In DeFi, once the liquidation transaction is confirmed on the blockchain, it’s final. However, some protocols now offer a grace period after unpausing or during extreme volatility, giving you a few hours to add more collateral or repay the loan before the liquidator acts.

What happens to leftover collateral after liquidation?

In DeFi, any leftover collateral after paying off your debt and fees is returned to your wallet automatically. In traditional loans, if the sale of your asset brings in more than what’s owed, the lender must return the surplus to you by law. But if the sale doesn’t cover the full balance, you may still owe the difference-called a deficiency balance.

Why do DeFi liquidation fees matter?

Liquidation fees are the discount liquidators get for paying your debt. If the fee is too high-say 30%-no one will bother because it’s not profitable. If it’s too low-say 2%-liquidators might act too slowly, letting bad debt pile up. Most protocols use 5% to 10%, balancing incentive and fairness. A fee that’s too high can destabilize the whole system.

Are SBA loan liquidations public record?

Yes. Details of SBA loan defaults and liquidations are reported to the National Guaranty Purchase Center and appear in lender filings. While personal information is protected, the loan status, collateral type, and recovery amount are public. This transparency helps prevent fraud and ensures lenders follow SBA rules.

10 Comments

DeFi liquidations are terrifying because they’re blind. No mercy, no grace, no second chances. One minute your ETH is worth $4K, the next it’s $3.8K and boom - your collateral’s gone. Traditional loans at least give you a phone call. DeFi? It’s like being in a car crash and the airbag deploys before you even hit the wheel.

LOL imagine being so broke you need to borrow against crypto and then panic when it dips 5%. 😂 You think you’re smart trading leverage until your whole stack gets auctioned off for 10% off. Welcome to the real world, champ.

The notion that DeFi is somehow more ‘efficient’ than traditional finance is a Silicon Valley fantasy. SBA loans may be slow, but they’re built on centuries of legal precedent - not code written by 22-year-olds who think ‘DAO’ is a type of sushi. Liquidation isn’t a feature; it’s a failure mode. And in DeFi, failure is instantaneous, irreversible, and utterly devoid of human dignity.

Meanwhile, in the real world, banks have compliance officers, auditors, and federal oversight. In DeFi, you’re at the mercy of a bot that doesn’t know what ‘empathy’ means. The whole system is a gamble with your livelihood, disguised as innovation.

And don’t get me started on the ‘grace periods’ they added after the 2023 flash crash. That’s not a feature - it’s damage control. The protocol was literally designed to fail, and now they’re slapping Band-Aids on a hemorrhage.

Traditional systems aren’t broken. They’re calibrated to protect people. DeFi is calibrated to maximize protocol revenue while offloading risk onto the least informed participants. That’s not finance. That’s predation with a blockchain.

When you hear someone say ‘decentralization means freedom,’ ask them if they’d trust a robot to take their house because the price of a digital token dipped too fast. If they say yes, they’ve never lost anything real.

DeFi liquidation fees are a delicate balance. Too low, and no one bothers to liquidate - debt piles up, protocol gets unstable. Too high, and liquidators can’t profit, so they sit idle. Five to ten percent is the sweet spot - enough incentive, not enough to break the system.

But here’s the thing: most users don’t even know what their liquidation threshold is. They see ‘borrow up to 75% LTV’ and think that’s safe. Nope. If ETH drops 30% in a day, you’re toast. No warning. No call. Just gone.

Set up price alerts. Use wallets with on-chain notifications. Never borrow more than half your collateral’s value. And never, ever use borrowed stablecoins to buy more crypto. That’s not investing. That’s Russian roulette with your life savings.

I appreciate how the post breaks down the human element in traditional lending versus the machine logic of DeFi. One system prioritizes fairness, the other prioritizes speed. Neither is inherently better - just different tools for different needs.

But I think we’re missing the bigger picture: the real innovation isn’t in the liquidation mechanics. It’s in the transparency. On-chain, you can see every transaction, every debt update, every liquidation. In traditional finance, you’re lucky if you get a letter in the mail before your car gets repossessed.

Maybe the future isn’t choosing one over the other. Maybe it’s blending them - using blockchain for auditability, but keeping humans in the loop for edge cases. That’s the kind of hybrid system that could actually work for everyone.

Did you know the SBA’s Form 1502 was designed by a committee that included ex-bank lobbyists? And the ‘National Guaranty Purchase Center’? It’s not a government agency - it’s a private contractor owned by a firm that also manages CLO tranches.

DeFi liquidations are scary? Sure. But at least you know who’s pulling the trigger. In traditional finance, the system is rigged from the top. The SBA guarantee? It’s a shell game. The real money is in the fees, the appraisals, the ‘recovery services’ - all funneled to the same few firms.

And CLOs? They’re designed to fail. The equity tranche is a sacrificial lamb. The whole structure is built so that when defaults happen, the big banks get bailed out while the small investors get wiped out. That’s not finance. That’s systemic theft.

DeFi is dangerous. But traditional finance? It’s a slow-motion Ponzi scheme with a federal seal on it.

People who say DeFi is ‘too risky’ are the same ones who cried when the 2008 crash wiped out their 401(k)s - but never questioned the banks that sold them toxic CLOs. Hypocrites.

At least with DeFi, you know the rules. No hidden fees. No fine print. If you don’t understand collateral ratios, don’t borrow. Simple. No one forced you to take a loan. No one lied to you.

Meanwhile, SBA loans? You think you’re getting help? Nah. You’re getting a trap. That ‘repayment plan’? It’s a 10-year debt sentence with interest that compounds in the background. And when you finally pay it off, your credit is ruined, your business is dead, and the lender made a profit off your misery.

DeFi doesn’t lie. Traditional finance lies with a spreadsheet.

Bro, just don’t borrow more than 50% of your collateral. Set alerts. Use a wallet that pings you. Boom. Done. 😎

As someone from India, I see this differently. In my country, people still use gold as collateral for loans - no apps, no blockchain, just a local lender and a receipt. It’s slow, but it works. People trust the human face, not the algorithm.

Maybe the real lesson here isn’t about DeFi vs traditional - it’s about trust. In the West, we’ve outsourced trust to machines. In places like mine, trust is still built in person. Both have flaws. But one lets you cry in the office and still get a second chance.

The post does a great job showing how each system reflects its cultural and institutional context. Traditional finance values process over speed. DeFi values speed over process. Neither is perfect, but both are responses to real human needs.

What’s missing is a discussion of emotional impact. Losing your home to a bank feels like failure. Losing your crypto to a bot feels like betrayal. The psychological weight is different - and we ignore that at our peril.

Maybe the future isn’t about choosing a system. It’s about designing one that doesn’t make people feel like they’ve been abandoned.