If you've tried to move your digital gains into a Russian bank account lately, you might have noticed things feel a lot more tense. It's not just your imagination. Since late 2025, the Russian banking system has shifted from a passive stance to an aggressive monitoring phase. Moving withdraw crypto to fiat funds is no longer a simple transfer; it's now a trigger for a sophisticated set of automated flags that can leave your cash locked and your account under a microscope.

The New Reality: Immediate Limits and Flags

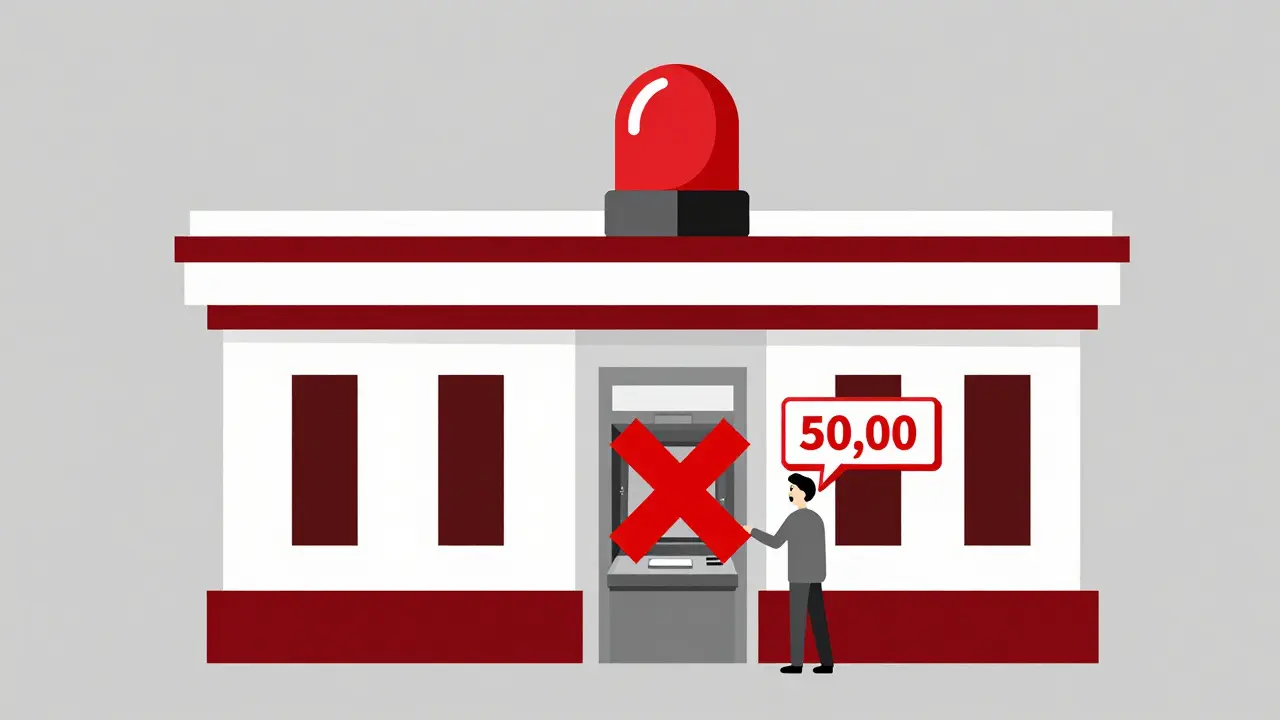

The biggest shock for most users is the implementation of Federal Law No. 3-1092818-2025 is a regulatory framework that allows Russian banks to immediately limit daily cash withdrawals to 50,000 rubles . If your transaction is flagged as suspicious, this limit kicks in for 48 hours. For many, this means being unable to access the bulk of their funds exactly when they need them most.

Banks don't just guess who is moving crypto. They use a precise set of 12 technical characteristics defined by the Central Bank of Russia (CBR) in Directive No. 74-P, which mandates the monitoring of specific transaction behaviors to detect unregulated crypto circulation . If you do any of the following, you're likely to trigger a flag:

- Withdrawing funds between 11:00 PM and 5:00 AM.

- Making withdrawals that aren't divisible by 1,000 rubles (e.g., withdrawing 10,542 rubles instead of 10,000).

- Using an ATM more than 50 kilometers away from your registered home address.

- Relying on QR codes or virtual cards instead of a physical plastic card.

- Receiving a transfer of over 200,000 rubles via the Faster Payments System and then trying to withdraw it within 24 hours.

The system is incredibly fast. If you're flagged, the bank is required to notify you via SMS or app within 15 minutes, and the 50,000 ruble cap is applied instantly. With 98% of the 347 licensed banks now using these systems, there are very few "safe" harbors left in the traditional banking sector.

Why Banks are Cracking Down

The Russian government's motivation is two-fold: stopping fraud and controlling capital. Governor Elvira Nabiullina has pointed out that nearly 89% of fraud cases in early 2025 involved cryptocurrency conversions. By making it harder to exit crypto into fiat, the state hopes to kill the incentive for scammers. Furthermore, the government is fighting a losing battle with capital flight; data shows that crypto accounts now facilitate over 37% of all cross-border currency withdrawals.

This creates a weird paradox. While the CBR is squeezing individual users, they are actually opening doors for big players. The Bank of Russia now allows domestic banks to engage in crypto operations, provided they cap their exposure at 1% of their regulatory capital and keep a 150% reserve ratio. Basically, if you're a massive institution, the rules are different; if you're a regular person using a P2P platform, the rules are strict.

P2P Platforms: The High-Risk Zone

If you use peer-to-peer (P2P) exchanges, you are in the crosshairs. The CBR specifically identifies transactions from platforms like Paxful or LocalBitcoins exceeding 100,000 rubles as high-risk. Because P2P involves receiving money from another individual (who might be a professional "changer" or a flagged account), banks often treat these incoming transfers as red flags for money laundering.

| Environment | Risk Level | Common Bank Reaction | Primary Trigger |

|---|---|---|---|

| P2P Exchanges | Very High | Account Freeze / 50k Limit | Transfers from unknown users |

| Centralized Exchanges | Medium | Request for Proof of Funds | Large, lump-sum deposits |

| Institutional Channels | Low | Standard Compliance | High capital reserves |

What Happens When Your Account is Frozen?

When the 48-hour limit isn't enough, banks may move to a full freeze. In these cases, you'll likely be asked to provide a notarized transaction history from your exchange. This is a nightmare for anyone using decentralized platforms (DEXs) because there is no central authority to provide a stamped document.

Users have reported that resolution times now average about 3.2 business days, and in many cases, you have to physically visit a branch-like Sberbank or VTB-to prove the source of your funds. These banks have expanded their monitoring teams by up to 400% since 2025, meaning there are more analysts than ever looking for reasons to flag your account.

Survival Strategies for Traders

Since the algorithms are looking for "unnatural" patterns, the best defense is to look like a normal bank customer. Legal experts suggest maintaining a "natural" transaction history for at least three months-regular spending on groceries, utilities, and transport-before attempting large crypto-to-fiat conversions.

Some traders use a "staggered" approach, spreading withdrawals across multiple bank accounts. While this can work, it's risky. Banks are increasingly sharing data, and if your activity looks like a coordinated effort to bypass the 50,000 ruble limit, you might trigger anti-money laundering (AML) algorithms that monitor cross-bank patterns.

The safest bet? Limit your conversions to known counterparties. Transactions with verified, long-term contacts have a 73% lower chance of being restricted compared to random P2P matches. Avoid the "night owl" withdrawals and stick to business hours to keep your activity under the radar.

The Road Ahead: Criminal Penalties and Digital Rubles

The pressure isn't letting up. There is legislation currently moving through the Duma that could introduce criminal penalties for people who repeatedly bypass these withdrawal restrictions. We're talking about potential prison time for "organized cryptocurrency conversion schemes." This indicates that the state is moving toward a full prohibition of unregulated crypto circulation by 2027.

The end goal is the Digital Ruble, which is scheduled for a phased rollout starting in September 2026. The government wants to push users away from decentralized assets and into a state-controlled digital currency where every single kopek can be tracked in real-time.

What is the current daily withdrawal limit for flagged accounts?

Under Federal Law No. 3-1092818-2025, banks can limit your daily cash withdrawals to 50,000 rubles for a period of 48 hours if your transaction is flagged as suspicious.

Why did my bank account freeze after a P2P trade?

P2P trades often involve transfers from unknown individuals. Banks use CBR Directive 74-P to flag these as high-risk, especially if the amount exceeds 100,000 rubles or if the transfer is followed by an immediate cash withdrawal.

What documents do banks ask for to unfreeze an account?

Banks typically require proof of the source of funds. This may include notarized transaction histories from your crypto exchange or documents proving legitimate income sources.

Is it safer to use multiple bank accounts for withdrawals?

While it can help avoid the 50,000 ruble limit on a single account, it can also trigger AML alarms if the banks detect a pattern of cross-institutional activity designed to evade restrictions.

Will these restrictions disappear when the Digital Ruble launches?

Unlikely. The Digital Ruble is intended to replace unregulated crypto circulation with a state-monitored system, meaning transparency and control will actually increase.

6 Comments

Oh please, like anyone actually believes these specific 'rules' about the time of day or the 1,000 ruble divisibility. It's just a random excuse they use to freeze accounts whenever they feel like it. The whole system is a joke and they're just making up numbers to keep people scared. Classic move to keep the peasants in line while the big banks play by their own rules. Absolute nonsense!

This sounds incredibly stressful for anyone just trying to manage their savings.

P2P is a minefield now...!!! You really need to use verified merchants only...!!! The risk of a chain-reaction freeze is way too high...!!! Always keep your funds fragmented...!!!

Honestly, if you're doing weird 3 AM transfers and then sprinting to an ATM 60km away, you're basically asking for it. Just be a normal person and you'll be fine. Why do people always try to game the system and then act surprised when the adults in the room catch them? It's not that hard to just follow the rules and stay out of trouble, really.

You have to understand that from a regulatory perspective, these flags are designed to catch high-velocity movement which is a hallmark of money laundering. If you're using DEXs, you're essentially operating in a black box, which is why banks demand notarized docs. My advice is to start building a credible financial profile now. Don't just dump a huge sum into an account that's been dormant for months. Use the account for small, daily purchases first. Create a pattern of legitimacy that makes a crypto transfer look like a minor event rather than a primary source of income. It takes patience, but it's the only way to avoid the AML algorithms. If you're already flagged, don't fight the bank in the app; go into the branch and bring every piece of evidence you have. Being human and transparent in person usually works better than an automated ticket. This is about risk mitigation, not just following a checklist. Be proactive with your documentation and you'll save yourself days of stress.

We need to be clear that these restrictions target the most vulnerable users who don't have access to institutional channels. It's a systemic failure when regular people are forced into high-risk behavior just to access their own money. The shift toward a state-controlled digital currency is a move away from financial autonomy and we should all be paying closer attention to how this blueprint might be applied in other regions. This isn't just a local issue; it's a lesson in how quickly digital freedom can be stripped away through 'security' frameworks.