Imagine needing a loan but being forced to lock up $150 worth of Bitcoin just to borrow $100. That is the reality of standard DeFi lending, a system where borrowers must provide more value in assets than they borrow to secure a loan. While this overcollateralization model keeps protocols safe, it wastes capital and locks users out if they don’t have enough crypto on hand. This is where non-standard collateral, unconventional asset types and mechanisms used as security for loans that deviate from traditional overcollateralized cryptocurrency assets comes into play.

Non-standard collateral allows you to borrow against your reputation, your identity, or even without upfront collateral at all. It’s the bridge between rigid blockchain code and flexible human trust. By 2025, analysts project these mechanisms could capture 15-20% of the total DeFi lending market. But with higher efficiency comes higher risk. Let’s break down how these systems work, who they are for, and what you need to watch out for.

Why Non-Standard Collateral Exists

The primary driver behind non-standard collateral is capital inefficiency. In traditional finance, you can get a mortgage or a personal loan based on your credit history and income. In early DeFi, protocols like Aave, a leading decentralized lending protocol launched in January 2020 and MakerDAO, the oldest major DeFi lending platform established in December 2015 required you to lock 125% to 150% of the loan value in volatile assets. If the price dropped, you got liquidated.

This created a barrier for two groups: institutions with real-world assets but limited crypto liquidity, and retail users with strong on-chain reputations but small portfolios. The Bank for International Settlements noted in 2022 that this model fosters "procyclicality," meaning markets become more unstable because everyone sells during downturns to cover loans. Non-standard collateral aims to fix this by allowing lower collateral ratios-sometimes as low as 20% for verified entities-or none at all.

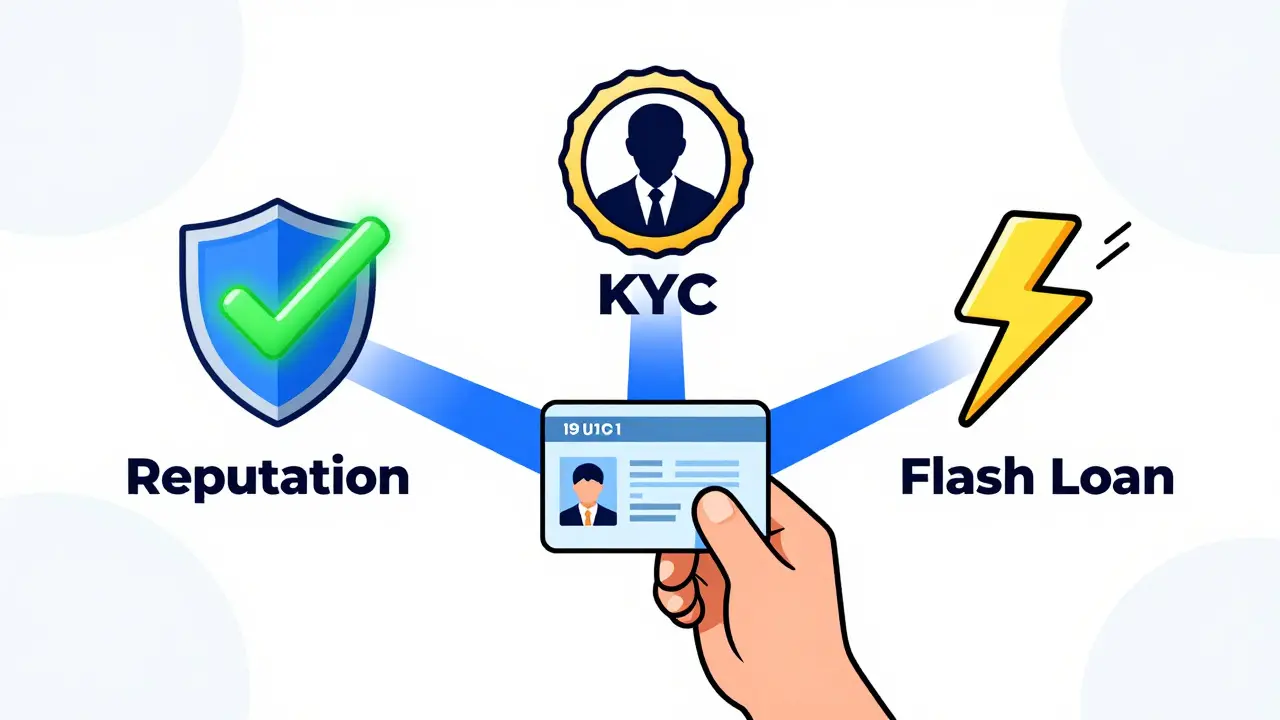

Types of Non-Standard Collateral Mechanisms

There isn’t one single way to do non-standard collateral. Instead, there are three main technical frameworks that have emerged since 2020.

- Undercollateralized Loans: These are loans where the collateral value is less than the loan amount, or zero. Platforms like TrueFi, an institutional lending protocol established in 2020 and Clearpool, a credit-based lending platform launched in Q4 2021 use this model. They rely heavily on Know Your Customer (KYC) checks and off-chain credit assessments. TrueFi, for example, offers institutional borrowers effective collateralization ratios as low as 20% after passing rigorous risk reviews.

- Reputation-Based Lending: Systems like Wing Finance, a reputation-based lending protocol launched in Q3 2020 analyze your on-chain behavior. They look at your transaction history across multiple protocols. To qualify, you might need six months of consistent activity and a minimum reputation score. This is essentially building a "crypto credit score" based on your past reliability rather than just your current balance.

- Flash Loans: Documented in Ethereum Improvement Proposal EIP-3151, flash loans allow you to borrow massive amounts of capital with zero collateral, provided you repay the loan within the same transaction block. Uniswap V2, a decentralized exchange facilitating approximately $6.2 billion in flash loan volume during 2022 is a key facilitator here. These are mostly used by sophisticated traders for arbitrage opportunities, not for buying coffee.

Risk vs. Reward: The Trade-Offs

You get better capital efficiency, but you pay for it with complexity and risk. Standard DeFi lending protocols experienced an annual default rate of only 0.3% during 2021-2022. In contrast, non-standard protocols registered a 4.7% default rate in the same period. Why? Because when markets crash, reputation scores drop, and unverified borrowers disappear faster than liquidation bots can react.

During the May 2022 market crash, non-standard collateral platforms saw default rates spike to 8.7%, compared to 3.2% on traditional platforms. Some protocols had to trigger emergency governance interventions. For instance, Alpha Homora triggered liquidations at -47% collateral ratios due to oracle lag-a situation that would be impossible in a standard overcollateralized pool.

| Feature | Standard Overcollateralized | Non-Standard Collateral |

|---|---|---|

| Collateral Ratio | 125% - 150% | 20% - 100% (or 0% for flash loans) |

| Borrower Verification | None (Anonymous) | KYC, On-Chain History, or Institutional Audit |

| Default Rate (2021-2022) | 0.3% | 4.7% |

| Primary Users | Retail Crypto Holders | Institutions, Traders, High-Reputation Users |

| Liquidity Access | High (if you have assets) | Moderate (limited by credit limits) |

Who Is This For?

Non-standard collateral is not yet a plug-and-play solution for the average retail user. As of Q3 2023, institutional users represent 68% of the non-standard collateral volume, with average loan sizes of $1.2 million. Retail adoption remains limited to 12% of volume, with average loans under $5,000.

If you are an institution or a high-net-worth individual, platforms like Maple Finance, an institutional lending protocol focusing on large-scale credit lines offer significant advantages. You can access liquidity without tying up your entire treasury in crypto. However, the process is slow. TrueFi requires full KYC/AML procedures that take 7-10 business days. Clearpool mandates a minimum six-month on-chain history with at least 50 transactions.

For retail users, the experience is mixed. Trustpilot reviews for Wing Finance show a 3.2/5 average rating. Users praise the accessibility for those without large holdings but criticize the "arbitrary" nature of reputation systems. One Reddit user reported securing a $50,000 loan with only 30% collateral but complained about the painful 15% interest rate. Another lost their entire $15,000 collateral when liquidation bots outpaced their repayment during a market dip.

Regulatory Landscape and Future Outlook

Regulators are watching closely. Dr. Gary Gensler, Chairman of the U.S. Securities and Exchange Commission, stated in October 2022 that undercollateralized DeFi protocols represent "significant systemic risk vectors." The Financial Stability Board warned in November 2022 that the absence of traditional credit underwriting standards creates counterparty risks that could amplify systemic vulnerabilities.

However, innovation continues. MakerDAO announced in July 2023 the integration of real-world assets, such as tokenized U.S. Treasury bonds, as non-standard collateral for DAI issuance. Aave introduced "isolated collateral pools" for non-standard assets in March 2023 to contain risk. The World Economic Forum predicts a gradual convergence between traditional credit infrastructure and DeFi-native mechanisms, with hybrid models becoming dominant by 2026.

Long-term viability depends on proving resilience through multiple market cycles. Messari analysts suggest that while non-standard collateral could reach $25-30 billion in total value locked by 2025, regulatory clarity remains the single largest determinant of growth.

How to Get Started Safely

If you want to explore non-standard collateral, treat it like learning to drive a manual transmission car-you need practice before hitting the highway. Here is a realistic checklist:

- Build Your On-Chain Resume: Start using standard DeFi protocols consistently. Maintain positive balances, repay loans on time, and interact with multiple dApps. Platforms like Clearpool look for at least six months of history.

- Understand the Risks: Read the documentation thoroughly. Understand dynamic liquidation thresholds. Unlike fixed-rate mortgages, your loan terms can change via governance votes.

- Start Small: Do not max out your credit line immediately. Test the mechanics with a small loan to understand the interface and the speed of liquidation bots.

- Verify the Platform: Stick to audited, well-established protocols. Avoid new launches promising "zero collateral" without clear risk mitigation strategies. Check for community support on Discord; response times matter during crashes.

- Consider KYC Requirements: If you are comfortable sharing identity information, institutional platforms like TrueFi offer better rates and higher limits. If you value anonymity, stick to reputation-based systems like Wing Finance, but accept stricter borrowing caps.

Non-standard collateral is reshaping DeFi, moving it from a purely mathematical game to a system that incorporates trust and identity. It’s powerful, efficient, and risky. Approach it with respect, and you might find new ways to unlock the value trapped in your digital assets.

What is non-standard collateral in DeFi?

Non-standard collateral refers to lending mechanisms in Decentralized Finance that do not require traditional overcollateralization (locking more value than borrowed). Instead, they use alternative security methods such as borrower reputation, on-chain history, identity verification (KYC), or instantaneous repayment structures like flash loans.

Is non-standard collateral safer than standard lending?

Generally, no. Non-standard collateral carries higher risk for lenders and often higher costs for borrowers. Data from 2021-2022 shows non-standard protocols had a 4.7% default rate compared to 0.3% for standard overcollateralized protocols. They are more vulnerable to market volatility and oracle failures.

Can I get a non-standard loan without any crypto?

It is difficult for retail users. Most non-standard loans still require some form of collateral, whether it is a small percentage of crypto, a strong on-chain reputation, or identity verification. Flash loans require no upfront collateral but must be repaid instantly within a single transaction block, making them unsuitable for general borrowing.

Which platforms offer non-standard collateral?

Key platforms include TrueFi and Maple Finance for institutional lending, Clearpool for credit-based lending, Wing Finance for reputation-based lending, and Uniswap for flash loans. Each has different requirements regarding KYC, on-chain history, and minimum loan sizes.

What happens if I default on a non-standard loan?

Consequences vary by protocol. In reputation-based systems, your on-chain reputation score may plummet, preventing future borrowing. In KYC-based systems, legal action or blacklisting may occur. In undercollateralized models, you may lose your remaining collateral, and in severe cases, the protocol may suffer losses if the collateral is insufficient to cover the debt.

8 Comments

The systemic risk vectors mentioned by the SEC are not merely theoretical constructs; they represent a tangible threat to financial stability that is often glossed over by enthusiasts. The reliance on off-chain credit assessments introduces a centralization point that fundamentally undermines the decentralized ethos of these protocols. Furthermore, the discrepancy in default rates between standard and non-standard collateral models highlights a critical vulnerability in the current risk mitigation frameworks. It is imperative that participants recognize the inherent fragility of reputation-based lending mechanisms when subjected to extreme market volatility.

hey tracy i get your point about the risks but look at the capital efficiency gains here. most people dont realize how much value gets locked up in overcollateralized loans just sitting there doing nothing. if you can borrow against your on-chain history or even just a small amount of crypto it opens up so many opportunities for growth. sure its risky but thats kinda the whole point of defi right? taking calculated risks for higher returns. i think the hybrid models coming in 2026 will be huge for this space

I completely agree with Brendan! The potential for capital efficiency is truly transformative, isn't it?! By leveraging undercollateralized loans, we can unlock liquidity that was previously trapped in static assets. This paradigm shift allows for a more dynamic allocation of resources across the DeFi ecosystem. Moreover, the integration of real-world assets like tokenized U.S. Treasury bonds as non-standard collateral represents a significant milestone in bridging traditional finance with decentralized protocols. We must remain optimistic about the regulatory clarity that will undoubtedly foster further innovation and adoption!

oh great another guide on how to lose your shirt in defi. 'build your on-chain resume' my ass. i spent six months being a good boy on clearpool and still got liquidated because some oracle lagged by three seconds during a dip. thanks for nothing abhishek. maybe if you actually understood how broken these systems are youd stop pretending its just about 'capital efficiency'. its about gambling with other peoples money and hoping the bots dont eat you alive first.

this article is boring. why do i need to read all this about flash loans and kyc when i could just buy memecoins and get rich quick? nobody cares about 'systemic risk' when the charts are green. also the author sounds like a robot. who writes like this anyway? 'non-standard collateral aims to fix this by allowing lower collateral ratios' yawn. i'm going back to sleep.

Ipsita, I understand your frustration with the technical jargon, but it is important to consider the long-term implications of these lending mechanisms! While meme coins may offer short-term excitement, they lack the fundamental structure that non-standard collateral provides for sustainable borrowing. Michael here, and I believe that educating ourselves on these topics is crucial for navigating the evolving DeFi landscape. Perhaps we can discuss the specific risks associated with reputation-based lending in more detail? It would be beneficial to explore how platforms like Wing Finance manage their risk profiles!

look everyone calm down. the default rate spike to 8.7% in may 2022 was definitely bad but its mostly due to oracle failures not the model itself. if you use platforms like truefi or maple you have to pass strict kyc which helps reduce the risk significantly. i've been using clearpool for a bit and while the interest rates are high the ability to borrow without locking up 150% collateral is worth it for me. just make sure you understand the liquidation thresholds before you dive in. dont max out your credit line immediately test it first

Aaron makes a solid point about testing small first. I've seen too many folks get wrecked by liquidation bots because they didn't pay attention to the dynamic thresholds. It's really helpful advice for anyone new to this space. The key is to treat it like learning to drive a manual car-you need practice before hitting the highway. Good luck to everyone exploring these options!